Indian Council for Research on International Economic Relations

Growth, Employment and Macroeconomy (GEM)

Trade, Investment and Economic Relations (TIER)

Agriculture Policy, Sustainability and Innovation (APSI)

Digital Economy, Startups and Innovation (DESI)

Climate Change, Urbanization and Sustainability (CCUS)

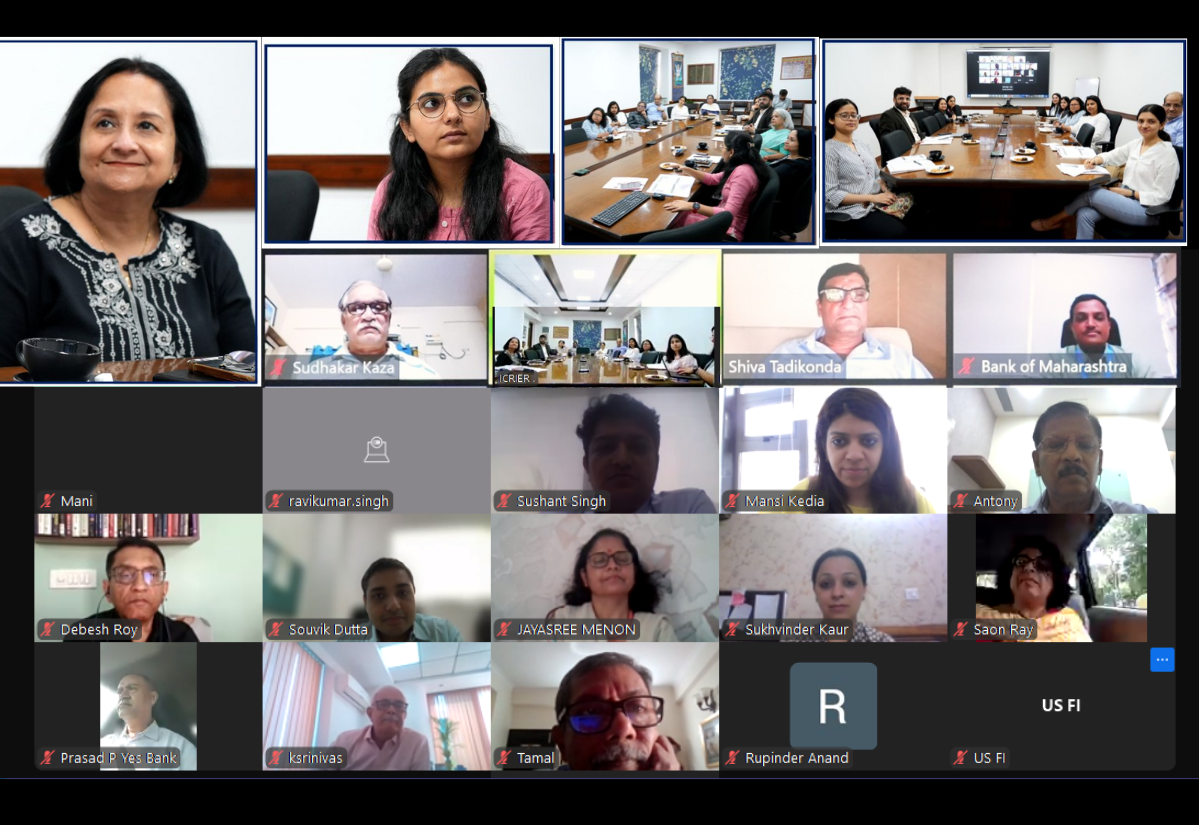

Closed-Door Consultation Role of ATMs in Financial Inclusion Date: April 18, 2024 (Thursday), Time: 03:00 PM Venue: Conference Room, ICRIER,...

@ 2024 ICRIER. All rights reserved.